Health insurance is a contract between you and a health insurance company. The agreement provides you with a health care plan to help you and/or your family pay for medical care.

However, when it comes time to use your health insurance, the details and nuances of these contracts can be quite confusing and leave you asking, “How does health insurance work?”

From understanding key health insurance terms to figuring out how much you’ll end up paying for services, keep reading to find out everything you need to know about how health insurance works, starting with the basics.

Key Takeaways

Health insurance can provide you and your family financial protection in case you need to use medical care services

Without insurance, health care can be expensive and unpredictable

There are different types of health insurance plans – it’s important to evaluate which plan will best meet your needs from a cost and design perspective

You can typically access health insurance through your employer, your spouse’s employer, or an individual plan

Why Do You Need Health Insurance?

Health care can be very expensive. Health insurance provides you and your family with financial protection if you need medical care services.

Even if you are a young, relatively healthy person, health care needs can often be unpredictable. It is important to have health insurance in case you get sick or need emergency care.

What Does Health Insurance Typically Cover?

Health insurance typically provides coverage for a variety of key medical services such as:

Preventive care – Your annual visit to your primary care physician

Primary care – If you have a cold (or feel ill) and need to see your primary care physician

Specialist care – Specialty doctor visits/consultations, such as cardiologists, endocrinologists, dermatologists, etc.

Inpatient / outpatient hospital care – If you are admitted to the hospital or need outpatient surgery (e.g., ACL repair)

Emergency services – Emergency room and transportation costs

Is it Mandatory to Have Health Insurance?

The short answer is, “it depends.” In 2019, the individual mandate, which required all individuals to have health insurance or pay a fee, was removed at a federal level. This means that individuals are no longer subject to a penalty if they did not elect health insurance.

However, some states chose to maintain the individual mandates, including Massachusetts, New Jersey, California, Vermont, Rhode Island, and Washington D.C. If you live in those states, you are required to have ACA-compliant health insurance.

Some states provide subsidies to lower-income residents who need help paying for this required coverage. The fees for not having coverage vary by state, so it would be best to check how your local state handles this policy.

Key Health Insurance Terms Explained

What are Health Insurance Premiums?

Health insurance premiums are the costs that you are required to pay to have access to health insurance. Health insurance premiums can vary based on who you include in your health insurance policy. Costs will be higher if you cover your spouse, domestic partner, or child(ren).

If you are offered health insurance through your employer, your employer may share the premium costs with you. Typically, health care through your employer will be cheaper than if you were to find health insurance on your own.

How Do Deductibles Work in Health Insurance?

A deductible is an amount that you will pay each year for eligible medical services or prescription drugs before your plan begins to cover some of the costs.

The deductible amount will be lower for those enrolled as an individual compared to those enrolled in a family coverage tier

Deductibles are also typically lower for in-network services versus out-of-network services

For example: If you had a deductible that was $1,000, you would need to pay $1,000 in claims before your plan kicks in. |

What is a Copay?

Copays are a flat dollar amount that you will pay at the time of receiving a specific service. If you have a plan with copays, you typically do not need to meet your deductible before copays apply. Copays may apply towards your deductible limit, but not always.

For example: You may have a $25 copay if you see your primary care physician. You would pay that amount at the time of service once the doctor’s office reviews your medical ID card details. |

What is Coinsurance?

Coinsurance is a portion of the medical cost that you will pay after you reach your deductible. Coinsurance is reflected as a percentage amount on your medical plan document. You pay a portion of the costs, and the health plan covers the remaining amount.

For example: Let’s say you need to receive lab or x-ray tests (and you already hit your deductible the prior month). If your coinsurance amount is 15%, you will pay 15% of those medical costs. The health plan will cover the remaining 85% of those costs. |

What are a PPO and HMO?

There are many types of health care plans available to individuals. Two of the most common medical plans are PPO plans and HMO plans.

PPO

PPO stands for preferred provider organization. This type of plan offers a network of providers from which you can get medical services. Costs are typically lower if you see a provider in the network, but you have the flexibility to go outside the network if you want to.

HMO

HMO stands for health maintenance organization. This type of plan only allows you to use their network of physicians and hospitals designated as in-network. If you were to see an out-of-network doctor, you would pay 100% of those non-contracted fees (this can be very expensive!). The only exception where out-of-network costs would be covered is in a true emergency.

PPO versus HMO

The most significant difference between a PPO and HMO is that the PPO plan offers more flexibility on which doctors you can see and when:

PPO plans allow you to seek care from in-network and out-of-network doctors (HMO plans only allow in-network coverage)

PPO plans do not require referrals from your primary care physician (PCP) to see a specialist – HMOs require members to obtain a referral from a PCP gatekeeper before receiving specialist care

HDHP

HDHP stands for a high deductible health plan. This type of medical plan is typically associated with having a higher deductible than traditional PPO or HMO plans but has a lower monthly premium. This means that you will need to pay a higher amount out-of-pocket for claims and services before your insurance kicks in.

The IRS has specific requirements for a plan to be a qualified HDHP:

One of the most beneficial aspects of enrolling in an HDHP is that you are eligible to open a health savings account (HSA). Those enrolled in an HDHP can contribute money into an HSA on a tax-free basis (up to specific annual maximums). Your HSA balance rolls over each year, and you can take it with you if you leave your employer.

If you are healthy and do not expect to need health care services, an HDHP might be the best option for you!

What are Out-of-Pocket Maximums?

An out-of-pocket maximum is the total amount of costs you will pay for medical services or prescription drugs in a given plan year. Once you hit that maximum amount, your health plan will cover 100% of all eligible health care costs for the rest of the plan year.

The out-of-pocket maximum amount will be lower for those enrolled as an individual compared to those enrolled in a family coverage tier

Your deductible, copay, and coinsurance payments count towards your out-of-pocket maximum limit throughout the plan year; monthly premiums do not

Out-of-network and in-network out-of-pocket maximums can differ; typically out-of-network out-of-pocket maximums are significantly higher

All plans that are in compliance with the Affordable Care Act (ACA) are required to have an out-of-pocket maximum in the plan design

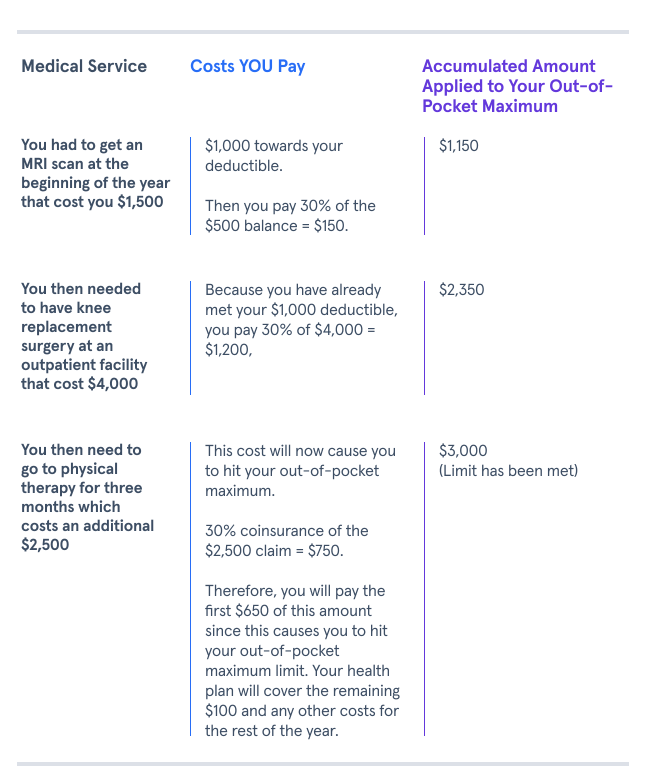

For example: Let’s say you have a deductible of $1,000, coinsurance of 30%, and an out-of-pocket maximum of $3,000.

How to Find the Right Plan for Your Needs

Choosing the right health care plan can feel overwhelming. Below are five key questions to ask yourself when selecting a plan:

Access to health insurance - Does my employer offer health insurance, or do I need to evaluate individual health plans on the state health insurance marketplace?

Monthly premium cost – Can I afford the monthly fee to have access to the plan?

Health care use – Do I expect to need a lot of medical care or prescription drugs in the upcoming year?

Out-of-pocket costs – How much will I pay for medical services if I need medical care? Can I afford these costs?

Plan network – Do I have access to in-network providers based on where I live?

Now that you’ve got the basics down on how health insurance works and the most common terms you’ll need to know, you can feel more confident when choosing and using your plan. The world of health insurance may seem complex, but with a solid understanding of the fundamentals, you can make better choices for your wellbeing (and your wallet)!